When we think of Health Insurance, we often visualize major hospital surgeries, intensive care units, and emergency room visits. But what about that nagging toothache or the root canal you’ve been putting off? For many, the dentist’s chair is the most common medical encounter, yet the question remains: does your Medical Insurance actually pick up the tab for your pearly whites?

In the evolving world of 2026, the answer is no longer a simple “yes” or “no.” As medical inflation rises, understanding the nuances of Dental Coverage is essential for any savvy policyholder. Whether you are looking for routine cleanings or emergency surgery, here is everything you need to know about dental care in the world of insurance.

1. The Short Answer: Is Dental Covered?

Generally, most standard Health Insurance Policies do not include routine dental procedures as a core benefit. Traditionally, insurance is designed to cover “In-patient Hospitalization”—meaning you need to be admitted to a hospital for at least 24 hours. Since most dental work is done in a clinic on an “Out-patient” (OPD) basis, it often falls outside the standard scope.

However, there are two major exceptions:

-

Accidental Injuries: If you are involved in an accident and require dental surgery as part of the trauma recovery, most policies will cover it.

-

OPD Riders: Many modern insurers now offer OPD Benefits or specific Dental Riders that you can add to your base plan for an extra premium.

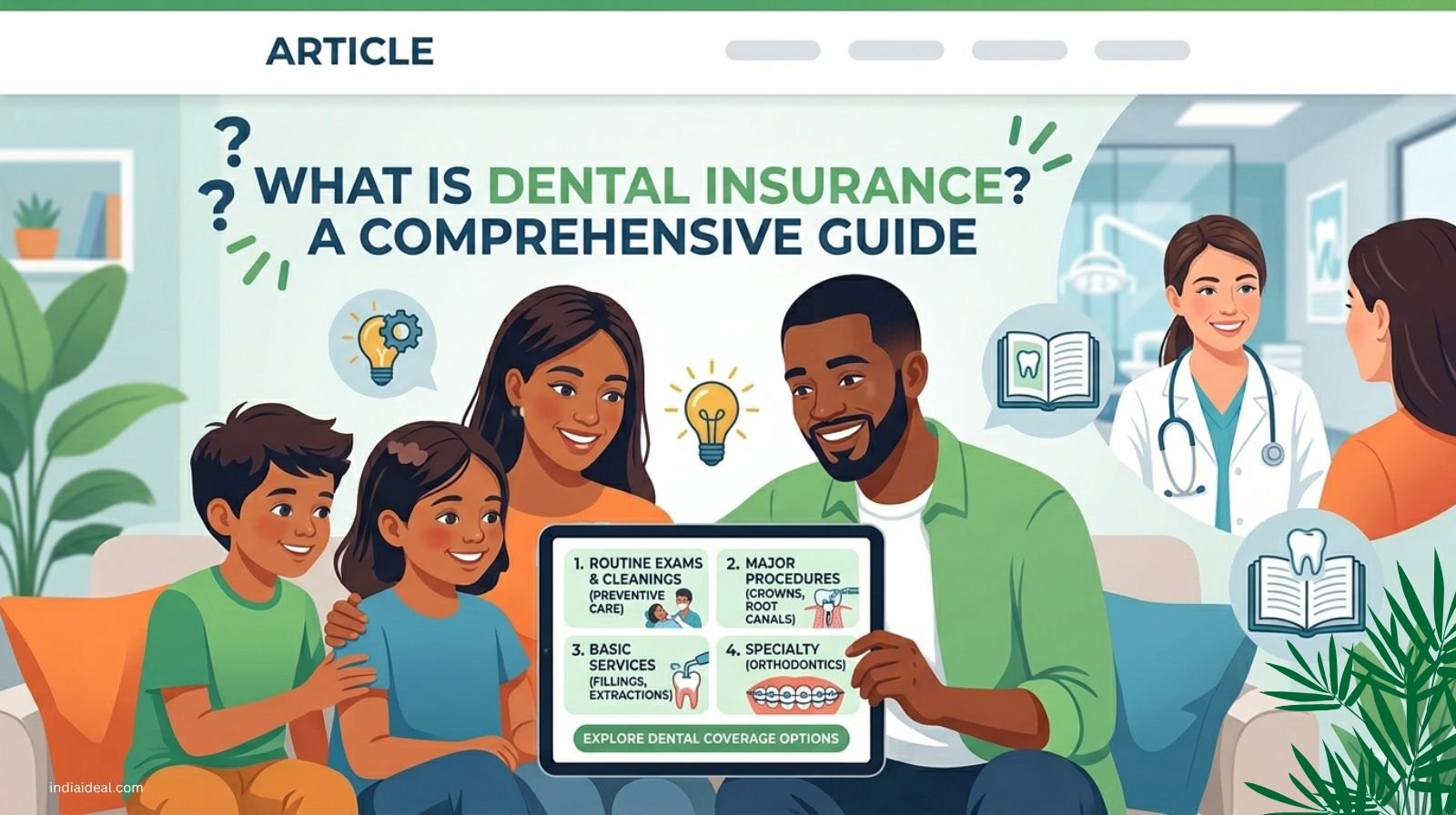

2. What Typically Gets Covered? (The Inclusions)

If you have a comprehensive plan or a specific Dental Add-on, here is what you can usually expect to be covered:

-

Accidental Dental Treatment: This is the most common inclusion. If a mishap results in a fractured jaw or broken teeth, the surgical repair is covered under Emergency Medical Care.

-

Root Canal Treatment (RCT): Some high-end plans now include RCT under their Outpatient Benefits, though often with a specific sub-limit (e.g., up to ₹5,000 or ₹10,000).

-

Extractions and Fillings: Basic procedures to remove a decayed tooth or fill a cavity are frequently covered in plans that offer OPD Coverage.

-

Diagnostic Services: Preventive measures like Dental X-rays and initial consultations are often part of wellness-oriented health plans.

-

Medically Necessary Surgeries: If a dental issue is a symptom of a larger problem, such as oral cancer or a severe cyst that requires hospitalization, it is typically covered under the base Health Insurance policy.

3. What is Usually Excluded? (The Fine Print)

Insurance is about “necessity,” not “vanity.” Therefore, insurers are very strict about what they won’t pay for:

-

Cosmetic Dentistry: Procedures like Teeth Whitening, veneers, or smile correction are almost never covered. These are viewed as elective aesthetic improvements.

-

Orthodontics (Braces): Unless it is for a child with a severe functional deformity, braces and aligners are generally excluded from Health Insurance Coverage.

-

Dental Implants: These are often considered “high-cost” and elective. Even the best policies usually exclude the cost of the implant itself unless it’s necessitated by a severe accident.

-

Pre-existing Conditions: If you buy a policy today to fix a tooth that has been rotting for two years, the insurer will likely reject the claim under the Pre-existing Disease (PED) clause.

-

Prosthodontics: The cost of dentures, bridges, and crowns is typically a self-paid expense.

4. Understanding OPD Benefits and Dental Riders

Since dental care rarely requires overnight hospitalization, the “secret” to getting your dental bills paid is the OPD Rider.

An OPD Benefit is an extension of your health insurance that pays for doctor consultations, pharmacy bills, and diagnostic tests that do not require hospital admission.

In 2026, many insurers are bundling Dental Care into these riders. While your main policy might have a Sum Insured of ₹10 Lakh, your dental OPD limit might be restricted to ₹5,000 or ₹15,000 per year. This is still highly valuable for covering the cost of annual check-ups and minor fillings.

5. The Waiting Period: Patience is a Virtue

Just like maternity or specific surgeries, Dental Coverage often comes with a Waiting Period. You cannot buy a policy on Monday and expect the insurer to pay for a root canal on Tuesday.

-

Standard Waiting Period: Most insurers impose a 12 to 24-month waiting period before you can claim for non-accidental dental procedures.

-

Accident Exception: If the dental work is required due to a sudden accident, the waiting period is usually waived from Day 1 of the policy.

6. How to Claim for Dental Expenses

The process for claiming Dental Insurance depends on whether the treatment was an emergency or a planned procedure.

-

Cashless Treatment: If your insurer has a tie-up with a network of dental clinics (like Clove Dental or similar chains), you can simply show your health card and get Cashless Claims settled directly between the clinic and the insurer.

-

Reimbursement: If you visit a private clinic outside the network, you must pay the bill upfront. Later, you submit the Original Bills, prescription, and the dentist’s report to the insurance company to get your money back.

-

Required Documents: Always keep your X-rays, the “Case Memo” from the dentist, and the detailed break-up of costs. Without these, the Claim Settlement process can become a headache.

7. The Rising Trend: Standalone Dental Plans

While still rare, some companies are now introducing Standalone Dental Insurance. Unlike a general health plan, these are “Discount Plans” or “Subscription Models.”

-

You pay an annual fee (e.g., ₹2,000).

-

In return, you get two free cleanings, free consultations, and a 20-50% discount on all major procedures like Dental Implants or RCTs.

-

These are excellent for families with children or seniors who know they will need frequent dental visits.

Why Dental Care Matters for Your Overall Health

Insurers are beginning to cover dental more frequently because they realize that Oral Health is a gateway to general health. Medical research has linked poor oral hygiene to:

-

Heart Disease: Bacteria from gum infections can enter the bloodstream and affect the heart.

-

Diabetes: Gum disease can make it harder for the body to control blood sugar.

-

Pregnancy Complications: Oral infections have been linked to low birth weight.

By covering Preventive Dental Care, insurance companies actually save money in the long run by preventing these more expensive chronic conditions.

Key Tips Before You Buy

Before you sign on the dotted line, ask your Insurance Agent these three specific questions:

-

Is there a Sub-limit on dental consultations?

-

Does the policy cover Root Canal Treatment under the OPD section?

-

Are there any network dental clinics in my city for Cashless Benefits?

Conclusion: Protect Your Smile and Your Wallet

While it is true that Dental Treatment isn’t always a standard feature in every health plan, the landscape is changing fast. In 2026, the best way to ensure your smile is protected is to look for Comprehensive Health Insurance that specifically mentions “Outpatient” or “Wellness” benefits.

Don’t wait for a toothache to start your research. A small investment in a Dental Rider today can save you tens of thousands of rupees tomorrow. After all, a healthy smile is an asset worth insuring!